Covering the energy world for Inside Energy means we run into words we don’t understand. On a daily basis? No, on an hourly basis. So, for our IE Questions postings we find terms to define or queries to answer as much for our knowledge base as for yours. Today, we’re looking at contango, and super contango.

A new dance fad? A super contango dance line, right?

Just like these Argentinian masters of the art?

No, it is not that much fun. It is much more esoteric and wonky.

Contango is a term thrown around by commodity traders and analysts. It is in such common usage that is also the name of a Houston-based oil and gas company and an assets management group.

A contango is what characterized the oil market up until a few weeks ago. The Financial Times puts it this way:

When the current price of a commodity, such as oil, is lower than prices for delivery in the future, the market structure in industry jargon is known as “contango”. This means it is attractive for traders to buy oil now at cheaper rates, store it, either on land or at sea, and sell it in time to come for higher prices and make a big profit. They lock in the profits by buying physical oil and selling forward on the futures market.

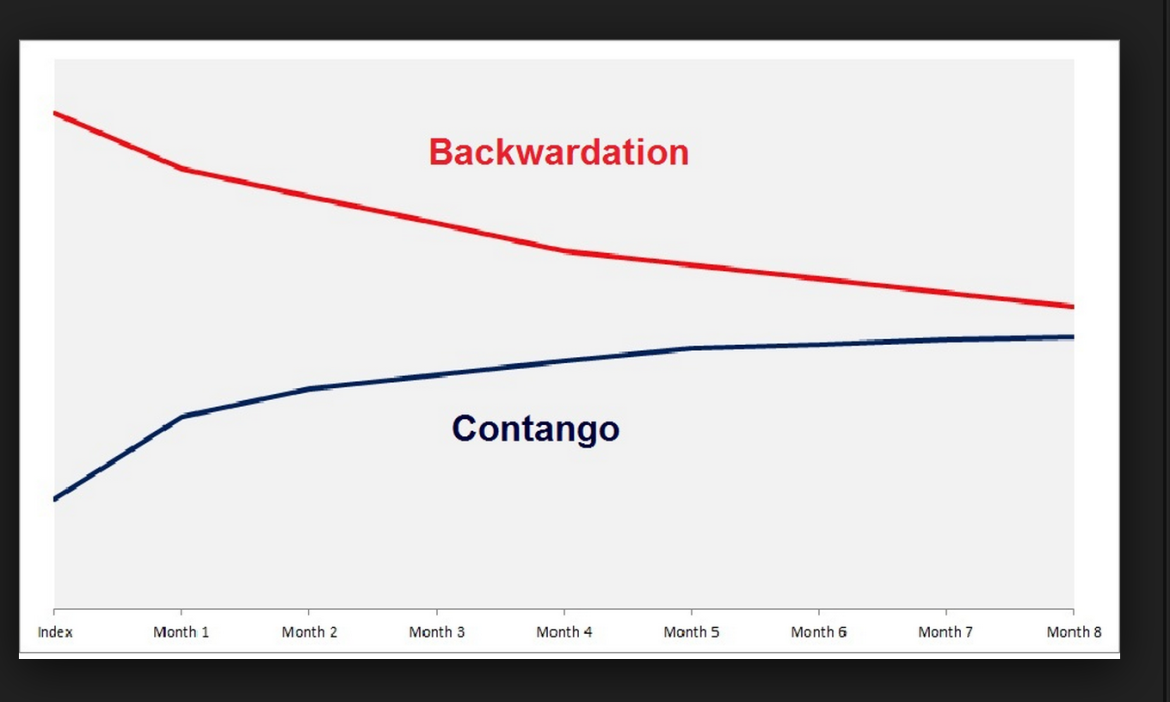

The opposite of contango is another curious term: “backwardation.” And this is what they look like on a chart:

Traders make money in a contango when the futures curve is steep enough to cover the cost of storing and insuring oil, either on shore or in supertankers, and still allow a profit to be made when the oil is eventually sold.

Remember back in March, when oil prices plunged below $44 per barrel? At that time there was a slew of stories about a crude oil glut, “overflowing” stockpiles of crude, and supertankers being bought up to store oil off shore to take advantage of …. a contango. In fact storage levels at that time were the highest since 1930. So, buy cheap now; sell expensive later.

Dance the contango!

I like the way this whole phenomenon is described by financial journalist Andrew Hecht in Seeking Alpha: “Last June, when … (the) oil price was above $107 per barrel, the market was in backwardation. Deferred prices were lower than nearby prices. This signaled tightness or more demand than supply. As the price moved lower, the backwardation narrowed and disappeared. By October, oil was in contango, which validated lower prices. The term structure moved from a condition of tightness to a condition that reflected the oversupply in the oil market, particularly in North America.”

At that time there was even concern that we were seeing another “supercontango” like the one in 2008 and 2009, during the financial crisis. At that time traders stored 100 million barrels at sea in supertankers.

Who wins the contango? Storage companies, of course, but also what’s known as “integrated oil companies,” like Shell or BP, who can extract oil AND store it themselves.

But all that contango talk has disappeared in recent weeks as oil prices have crept upward once again, and storage supplies have crept down. The contango in one-year crude oil spreads has recently dropped from over 20% to under 7% because of higher prices.

If you want to dig into the etymology of the terms “contango” and “backwardation,” check out the Bloomberg’s explanation here.